An advance salary is the payment given to an employee before the actual payday. It is usually provided when an employee requests part of their salary in advance due to personal or financial needs. From an accounting perspective, this transaction must be properly recorded to ensure accurate financial statements and clear tracking of liabilities.

In accounting books, advance salary is treated as an asset for the employer until it is adjusted against the employee’s future salary. Proper journal entry recording helps maintain transparency, avoids confusion in payroll processing, and ensures compliance with accounting standards.

What is Advance Salary?

Advance salary refers to a portion of an employee’s salary that is paid before the regular payment date. This amount is later adjusted from the employee’s monthly salary. It is not an additional expense for the company but rather an early payment of a future liability.

For example, if an employee’s monthly salary is 50,000 and the company gives 10,000 in advance, then this 10,000 will be deducted from the upcoming salary. This ensures that the company does not bear extra cost but simply adjusts the timing of payment.

Accounting Treatment of Advance Salary

In accounting, advance salary is recorded as an asset because the company expects to recover it by deducting it from future salary payments. It is usually shown under the heading “Advance Salary” or “Prepaid Salary” in the balance sheet.

When the salary is finally paid, the advance amount is adjusted, and only the remaining salary is recorded as an expense. This ensures that financial statements reflect the correct expense for the accounting period.

Journal Entry for Advance Salary

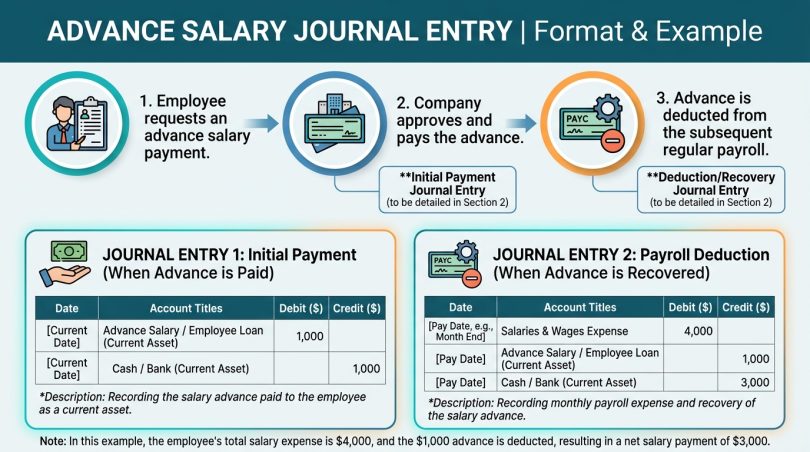

When advance salary is paid, the following journal entry is recorded:

Advance Salary Paid Entry:

Advance Salary A/C …… Dr

To Cash/Bank A/C

This entry shows that the company has given money in advance, which becomes an asset. Cash or bank balance is reduced, while advance salary is recorded as receivable from the employee.

Journal Entry at the Time of Salary Adjustment

When the actual salary is paid, the advance amount is adjusted. The entry is:

Salary A/C …… Dr

To Advance Salary A/C

To Cash/Bank A/C

This entry shows that the total salary expense is recorded, the advance is adjusted, and the remaining amount is paid to the employee.

Example of Advance Salary Entry

Let’s assume an employee receives a monthly salary of 40,000. The company gives 10,000 as advance salary.

Step 1: Advance Salary Paid

Advance Salary A/C …… Dr 10,000

To Bank A/C 10,000

Step 2: Salary at Month End

Salary A/C …… Dr 40,000

To Advance Salary A/C 10,000

To Bank A/C 30,000

In this example, the employee receives 10,000 in advance and 30,000 at the end of the month. The total salary expense remains 40,000.

Importance of Recording Advance Salary

Proper recording of advance salary is important for maintaining accurate financial records. It helps businesses track how much salary has already been paid and how much is still payable to employees.

It also prevents errors in payroll management and ensures that financial statements reflect true expenses. Without proper entries, companies may face confusion in salary calculations and reporting.

Key Points to Remember

Advance salary is not an additional expense; it is an early payment of salary. It is recorded as an asset until adjusted. Proper journal entries must be passed at the time of payment and salary settlement.

It is important for accountants to ensure accuracy in these entries to maintain clear financial records. This also helps in smooth payroll processing and avoids discrepancies in employee payments.

Conclusion

Advance salary journal entries are an essential part of payroll accounting. They ensure that early salary payments are properly recorded and adjusted in financial statements. By treating advance salary as an asset and correctly updating it during salary processing, businesses can maintain accurate and transparent accounting records.

Understanding the format and examples of these entries helps students, accountants, and business owners manage payroll more effectively and avoid common accounting errors.