Introduction

In accounting, recording business transactions accurately is one of the most important tasks. One such common transaction is the purchase of goods. Whether a business operates on a small scale or manages large inventories, every purchase must be properly recorded in the books of accounts. This is done through a journal entry.

Understanding how to pass a journal entry for purchase of goods helps maintain accurate financial records, track inventory, and prepare financial statements correctly. In this article, we will explore the concept in detail, along with types, rules, and practical examples.

What is a Journal Entry for Purchase of Goods?

A journal entry for purchase of goods is the process of recording goods purchased by a business in its accounting books. These goods are usually bought for resale or for production purposes.

In simple words, when a business buys items to sell them later, it must record the transaction in the journal book using debit and credit rules.

The entry depends on how the goods are purchased—whether in cash or on credit.

Meaning of Goods in Accounting

Before learning journal entries, it is important to understand what “goods” means in accounting.

Goods refer to items that a business buys for the purpose of selling them again. These are different from assets like machinery or furniture, which are used for long-term purposes.

For example:

- A clothing shop buys shirts to sell → Goods

- A factory buys raw cotton → Goods

- A company buys a computer for office use → Not goods (it is an asset)

Types of Purchase Transactions

There are mainly two types of purchase transactions:

1. Cash Purchase of Goods

When goods are purchased and payment is made immediately, it is called a cash purchase.

Example: A shop buys inventory worth $1,000 and pays cash instantly.

2. Credit Purchase of Goods

When goods are purchased but payment is made later, it is called a credit purchase.

Example: A business buys goods worth $2,000 from a supplier and agrees to pay after 30 days.

Both transactions require different journal entries.

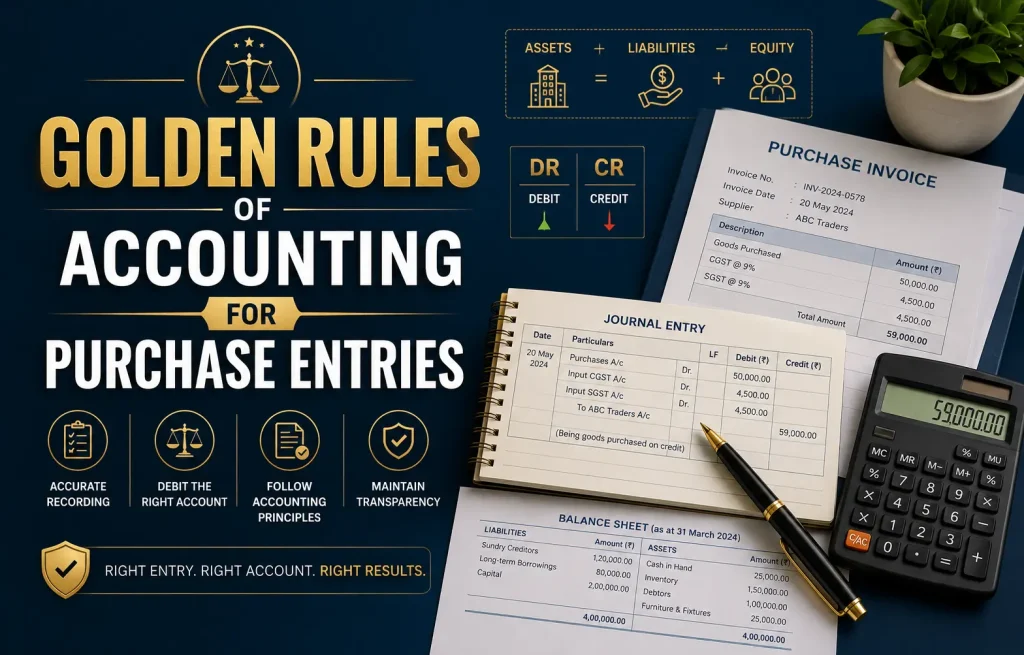

Golden Rules of Accounting for Purchase Entries

To pass correct journal entries, we use the golden rules of accounting:

For Real Accounts (Goods/Inventory)

- Debit what comes in

- Credit what goes out

For Personal Accounts (Suppliers/Creditors)

- Debit the receiver

- Credit the giver

For Cash Transactions

- Cash account decreases → Credit cash

These rules help decide which account to debit and credit.

Journal Entry for Cash Purchase of Goods

When goods are purchased for cash, the inventory increases and cash decreases.

Journal Entry:

Purchases Account Dr.

To Cash Account

Explanation:

- Purchase account is debited because goods come into the business

- Cash account is credited because cash goes out

Example:

A business buys goods worth $5,000 in cash.

Journal Entry:

Purchases A/c Dr. 5,000

To Cash A/c 5,000

Journal Entry for Credit Purchase of Goods

When goods are purchased on credit, the business owes money to the supplier.

Journal Entry:

Purchases Account Dr.

To Supplier’s Account (Creditor)

Explanation:

- Purchases are debited because inventory increases

- Supplier is credited because liability is created

Example:

Goods worth $8,000 are purchased from ABC Traders on credit.

Journal Entry:

Purchases A/c Dr. 8,000

To ABC Traders A/c 8,000

Purchase of Goods with GST or Tax

In modern accounting, taxes like GST (Goods and Services Tax) are often included in purchase entries.

Example:

Goods purchased for $10,000 with 10% GST.

- Goods value = $10,000

- GST = $1,000

- Total payment = $11,000

Journal Entry:

Purchases A/c Dr. 10,000

Input GST A/c Dr. 1,000

To Cash/Bank A/c 11,000

This shows tax separately for better financial reporting.

Purchase Return (Goods Returned to Supplier)

Sometimes purchased goods are returned due to defects or other reasons. This is called purchase return or return outward.

Journal Entry:

Supplier Account Dr.

To Purchase Return Account

Example:

Goods worth $2,000 returned to supplier.

Supplier A/c Dr. 2,000

To Purchase Return A/c 2,000

This entry reduces purchases and liability.

Importance of Recording Purchase Journal Entries

Proper recording of purchase transactions is essential for several reasons:

1. Accurate Financial Records

It ensures that all purchases are properly tracked in the accounting system.

2. Inventory Management

Businesses can monitor stock levels effectively.

3. Profit Calculation

Correct purchase data helps calculate accurate profit and loss.

4. Tax Compliance

Proper entries help in GST or tax reporting.

5. Decision Making

Business owners can analyze purchasing trends and control expenses.

Common Mistakes to Avoid

Many beginners make mistakes while recording purchase entries. Here are some common ones:

1. Confusing Assets with Goods

Only items purchased for resale are recorded as goods.

2. Wrong Account Selection

Using incorrect accounts can lead to inaccurate financial reports.

3. Not Recording Credit Purchases Properly

Ignoring creditor accounts can misrepresent liabilities.

4. Mixing Expenses with Purchases

Expenses like rent or salary should not be recorded as purchases.

Simple Practice Examples

Let’s understand more with examples:

Example 1:

Bought goods for cash $3,000.

Purchases A/c Dr. 3,000

To Cash A/c 3,000

Example 2:

Bought goods on credit from XYZ Ltd. $6,500.

Purchases A/c Dr. 6,500

To XYZ Ltd. A/c 6,500

Example 3:

Returned goods worth $500 to supplier.

XYZ Ltd. A/c Dr. 500

To Purchase Return A/c 500

Difference Between Cash and Credit Purchase Entry

| Basis | Cash Purchase | Credit Purchase |

|---|---|---|

| Payment | Immediate | Later |

| Credit Impact | None | Liability created |

| Account Credited | Cash | Supplier |

| Risk | Low | Higher |

Role of Journal Entry in Accounting System

Journal entries form the foundation of accounting. Every financial transaction starts with a journal entry before moving to ledger accounts and financial statements.

Without proper purchase entries:

- Inventory records become inaccurate

- Profit calculation becomes wrong

- Balance sheet may not match

Conclusion

Recording a journal entry for purchase of goods is a fundamental accounting process that ensures accurate financial tracking. Whether goods are purchased in cash or on credit, each transaction must be properly recorded using debit and credit rules.

Understanding these entries not only improves accounting knowledge but also helps businesses manage inventory, expenses, and profits efficiently. With practice, anyone can master this essential concept and apply it in real business situations.